Being financially uneducated is expensive.

Many of us had to learn about money the hard way, incurring debt along the way, but it doesn’t have to be that way for your child. You can give your child the knowledge they need to make wise financial decisions before they get access to easy credit.

By teaching kids about money, you can help them avoid costly mistakes that lead to wasted time and money. Time and money that could be spent on building a life of wealth and abundance.

{This post contains paid links. Please see disclaimer.}

You may have taught your child the foundations of personal finance but they’re going to need to be familiar with bigger concepts such as debt, borrowing, mortgages and investing basics if they’re going to get ahead financially. It may sound advanced but kids are hungry to understand how the world around them works. By teaching your child these key financial concepts you’re giving them the head start in life they need.

When children understand how the financial system works and how to use it to their advantage they’re able to feel confident about money and the future.

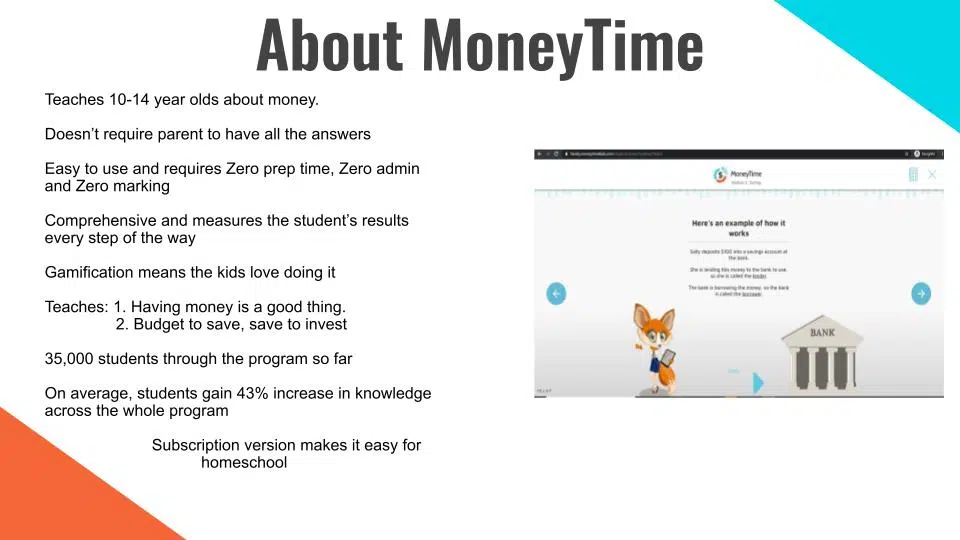

Are you looking for an online financial literacy course for your homeschool? MoneyTime will teach your child all the things you wish you had been taught about money.

That’s why I’m so excited to share today’s interview with Neil Edmond, founder of MoneyTime, on this week’s Homeschool Conversations podcast episode! A big thank you to MoneyTime for sponsoring this episode and post.

Be sure to check out all the other interviews in our Homeschool Conversations series!

Watch the video. Listen to the podcast. Read the show notes. Share with your friends!

Who is Neil Edmond of MoneyTime?

A former business consultant for 20 years, Neil has helped thousands of people improve their financial outcomes. Neil has 3 children in their late teens and early twenties and is concerned their generation are growing up with limited financial literacy and has decided to do something about it. Neil is the designer and author of MoneyTime which has been used by over 35,000 10-14 year old students in the US, Australia and New Zealand.

{This post contains paid links. Please see disclaimer.}

Watch my interview with Neil Edmond

Prefer to listen to your content? Subscribe to Homeschool Conversations on Apple podcasts or wherever you get your podcasts so you don’t miss a single episode!

Amy: Hello, everyone, I am delighted to be joined today by Neil Edmond. Neil is a former business consultant for 20 years and he has helped thousands of people improve their financial outcomes. Neil has three children in their late teens and early 20s and is concerned their generation is growing up with limited financial literacy, but he’s decided to do something about it. Neil is the designer and author of MoneyTime, which has been used by over 35,000 10 to 14-year-old students in the US, Australia, and New Zealand. Neil, I’m delighted to get to chat with you today.

Neil: Thank you, Amy. It’s a pleasure to be on your show.

Amy: Here at the beginning, could you just tell us a little bit about yourself and your family and your own personal background?

Neil: Sure. I’m 55 years old, and I live in Christchurch, New Zealand, a long way away from where you are right now. It’s a small world these days, full of internet connectivity and that sort of thing. Here we are. Christchurch, you may know, was pretty much leveled in a major earthquake about 10 years ago. We lost 80% of the buildings in our central business district. The city is gradually being rebuilt. It’s starting to look wonderful. It’s a bright, new modern city.

We’re really starting to enjoy being back in the modern world again, rather than kicking around in piles of rubble. It’s a wonderful place to live.

As you said, I’m married, I’ve got three kids, they’re all a college at the moment. Monique, my wife and I, we’re empty nesters at the moment for the first year. We’re kind of enjoying that, we miss the kids but it also gives us more opportunity to do things we enjoy doing like mountain biking and hiking and going to movies. That’s pretty much how I spend my life these days.

Amy: What about your own background in the financial world?

Neil: Sure. Most of my experience and finance is just self-taught. I wasn’t taught when I was a kid. Unfortunately, my father died when I was quite young and that certainly wasn’t my mother’s strength. I learned a lot of the stuff that I know through trial and error, then got to fill in the gaps through reading books and listening to podcasts and doing webinars, that sort of thing.

That’s served me pretty well recently, but like a lot of people, I made some big mistakes early on and they’re mistakes that I really didn’t want my kids to be making the same mistakes.

I asked them, “What are you being taught at school about financial literacy?” The answer came back, “What’s financial literacy?” They just literally weren’t being taught anything. I thought, “Well, gee, we need to do something about this.”

I’d had a good run with my consultancy, I’d been doing it for 20 years, decided I wanted to leave a legacy. I thought, “Great, well, I’ll just write a program for kids, teach them financial literacy and see how that goes.” Four years later, here we are, we’re in four different countries and lots of kids using it. It’s been a blast.

Why teach our children to understand money and finances?

Amy: I think so many parents can relate to what you’re saying. They didn’t have a good foundation given to them and they came into adulthood, made a bunch of mistakes. They’re looking back now and they’re looking at their children and they’re thinking, “I want better for them. I don’t want them to have to make all those same mistakes I made. We can learn the hard way or we can learn the easier way.” We want that easier way for our children. Here at the beginning, we’ve kind of touched on it a little bit, but let’s go big picture. Why is it important for our children to understand money and finances?

Neil: Why is financial literacy for kids so important?

Well, these days, kids are exposed to a lot of advertising and they’re also subject to a lot of peer pressure, which means that they end up wanting to spend and actually spending a lot of their money straight up without any consideration for the future or what that might look like. They’re growing up in an age of instant gratification.

We as parents tend to want our children to have a better life than what we had. We don’t want them to have to struggle as much as we did. We tend to give them money more freely than perhaps we were as youngsters. They have this expectation of instant gratification, which means they go out and spend but they end up developing bad spending habits, they spend beyond their means. Because the money is there, they believe it always will be there.

The consequence of that is that they end up building up debt. That debt can take the forms of credit cards when they get a bit older, personal loans, after-pay. Debt is a real killer when you’re starting out.

When kids– we’re specifically talking about, I guess, teenage kids here. What we’re trying to do is build good habits at this point, because once they leave school, if they haven’t got good habits and attitudes towards money in place by then, that’s when the debt really starts to become a killer. If they’re overspending, going into debt, they should be spending that time creating money, building wealth, doing jobs, saving money, and then investing it, then build up their net wealth so then they’re really well placed to buy a house, to further their education, to have a family, buy a business. But you can’t do those sorts of things if you’re struggling to pay off debt.

The other thing that it has a big impact on obviously is the credit scores. It’s going to be very hard for them or makes it a lot harder for them to do things like buy houses, or cars, or businesses if their credit scores been affected by their inability to pay off their debts.

It’s really important that they have these good attitudes and behaviors early on so that they are in the mode of earning to save and then saving to invest in their early 20s.

This is particularly important in this day and age, with the cost of housing becoming so rampant. The cost of housing is rapidly outstripping wage growth and it’s making it really difficult for young kids to get their own property. If that’s an aspiration, for most of us it is, then we need to be putting them in a situation or they need to be in a situation where they can actually afford the collateral to buy a house, if they want to do that. They shouldn’t be in debt, they should actually have been accumulating wealth to achieve that.

What we need to do is teach them how to earn, budget, and save, so that they can either invest in something, or they can start up and/or buy a successful business.

Amy: This past weekend in the car with my kids, we were talking about a certain circumstance and talking about how hard that would be, how long it would take to pay off the debt for that kind of purchase, or if you were in that situation. My teen daughter spoke up and she was like, “The easiest way is just not to get in debt in the first place.” I was like, “Yes, I’ve done something right. That’s exactly it.”

Neil: That’s brilliant, well done. I’m a really big fan of not letting kids have credit cards. If they never start with one, then they’ll never have issues with one. You can certainly live life pretty comfortably and effectively and easily without a credit card. If they can avoid that to start with, then they’re off to a good start.

Amy: I just wanted to mention to those of you who are watching the video, or listening to the audio that Neil has prepared some slides and some really helpful notes. As you’re listening to our conversation, if you’re driving or running or cooking dinner, and you don’t have time to stop right now and take notes, don’t worry, you’ll be able to access all of this information in the show notes for this episode over at www.humilityanddoxology.com. You can just listen and absorb this conversation as we go.

Laying a foundation of financial literacy in the early years

Neil, the next question I wanted to ask you was as we’re talking about young children, let’s focus on those beginning years as we’re laying a foundation for financial literacy. What are some practical ways we can begin teaching our children to think wisely about money even when they’re very young?

Neil: Absolutely. I’ll get on to what you can do to teach your kids in a bit but to answer the question regarding can we teach young children about money? The answer is yes, absolutely.

I guess a question a lot of parents ask me is, when? When is the best time to start teaching them? Is it when they start to count? Is it when they start getting an allowance? Is it when they’re about to leave school?

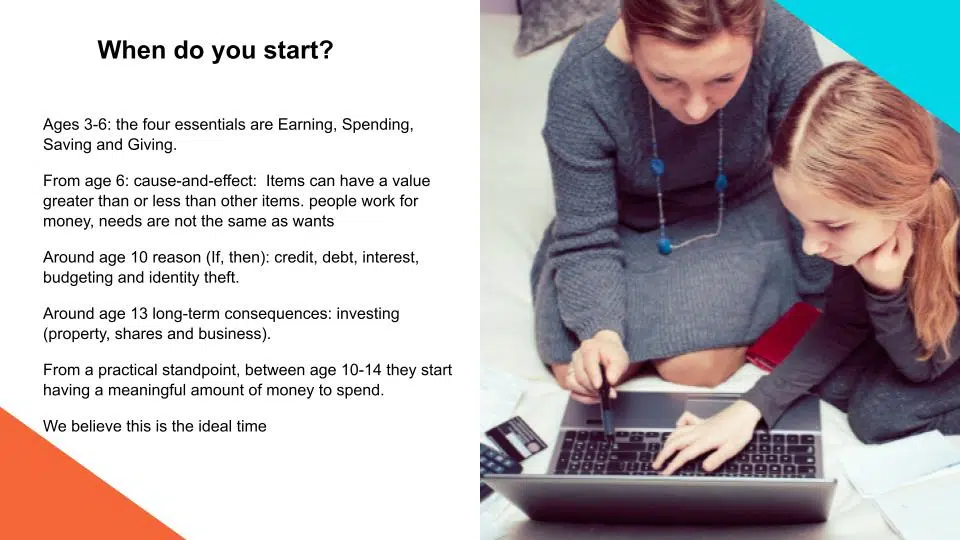

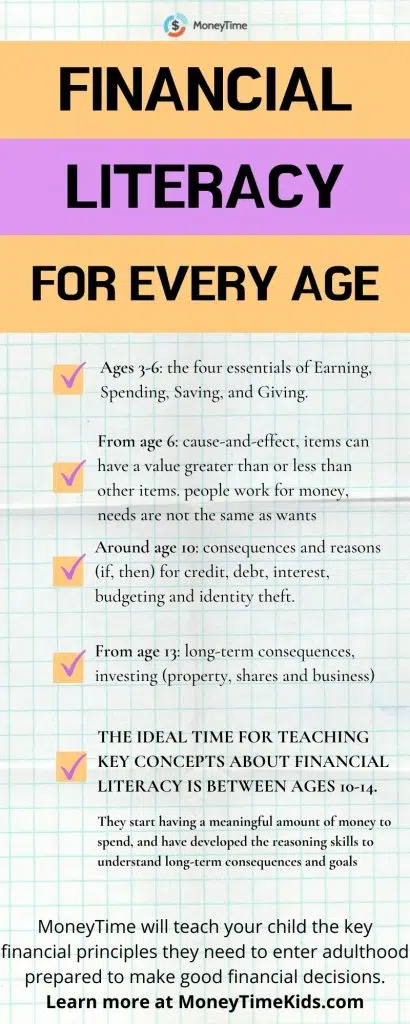

Ages 3-6

There’s quite a lot of research out there especially from universities in the States about the learning ability of kids at various times in their lives. What they’ve discovered is that in the ages of say three to six, they’re just starting to get going with their thought processes and starting to understand how the world works. During that stage, and personally, I would think from about five or six onwards, you can start teaching them simple concepts like earning, spending, saving, and giving, and they’re certainly capable of understanding that.

Ages 6-12

From six onwards, you can start looking at the cause and effect of things. Some examples of these items can have a value greater or less than other items. You can talk to them about the fact that people work for money. It just doesn’t appear. That it has to be earned. That’s a lesson that kids quite often don’t get even when they’re older.

You can discuss things like needs are not the same as wants so that they can understand those sorts of concepts, sort of ages 6 to 10.

Then around about 10 years old, they start to develop more reasoning capability.

I raised this or think of it in terms of if I go into debt, then I have to pay it back. Or if I borrow money, I have to pay interest. Or if I do a budget, I can have money left over at the end of the week. Or if I give my details out to somebody on the internet that I shouldn’t have, then there are consequences of that. That all happens around about the age of 10. They understand those sorts of things.

Ages 13+

Then after 13 or so, they’re getting a lot better at understanding long-term consequences if they do something now that’s going to have an impact on them in the future. That’s a good time to start talking to them about investing. If you put money into an investment now, it’s going to grow and it’s going to be a lot, but yes, hopefully in the future. You can talk to them about property and shares in business.

There’s quite an age range there. We’ve covered ages 3 through 13.

Ages 10-14: the Financial Literacy Sweet Spot

From a practical standpoint, the ages between 10 and 14 are when they start having a meaningful amount of money of their own through allowances or chores or jobs or gifts from family, birthday presents, et cetera. That’s when they’re starting to learn the purchasing power of money, their ability to go out and acquire things that they want.

We think that that’s the best age to really be drilling down into some of these financial literacy concepts and teaching them about the basics. They’re old enough to understand, they’re old enough to experience that for themselves, and we think that’s the best time to be building good habits and attitudes around money.

Amy: That’s really helpful to hear those different ages and stages of how children are going to be thinking. I have five children and each of them, in one of those stages. My youngest little guy is six and he just loves Lego and he wants Lego all the time. He’s always asking for Lego and we always have to remind him, “Do you have any money to buy the Lego?” He got some birthday money, and just even that process of sitting down with mom, realizing he had a finite amount and he had to choose. He could only pick one thing. That lesson of when you choose to use your money in one way, you don’t have it to use for something else. He’s still learning that. He’s still getting that but that was a good opportunity to practice that with him.

Neil: Sure. That’s a fun age to be teaching kids that sort of thing. I think a lot of parents who are engaged with their kids will naturally find this comes quite naturally because it’s just normal life. It’s just real-life experience. You don’t have to be a financial wizard to teach them the basics. We all know them. We all have to learn them ourselves. Because you can relate it to everyday experiences. You’re going grocery shopping, to go and buy some clothes, or you to do some activities that you’re naturally doing anyway. You can just develop a conversation with them, just include them in the experience. Then they pick up stuff. They’re like sponges, as you know. They just pick up at that as you go along. It’s not actually that hard to teach them the basics from early.

Practical ways to teach financial literacy concepts to children

Amy: Neil, what are some other practical ways that we can be teaching these concepts to our children?

Neil: That’s a great question.

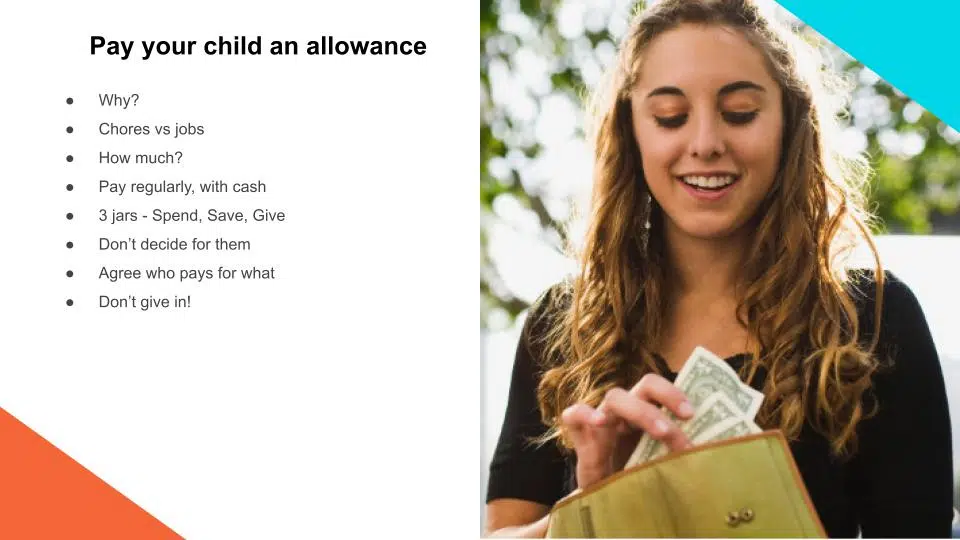

Paying children for their work around the house (chores, allowances, jobs, and more)

I think the first thing that you should look to do or parents should look to do is pay your child an allowance. I know that’s controversial for some people but just hear me out on this.

If kids can earn money when they’re younger, they learn the value of money and they learn the value of work.

If they’re having to do something to earn the money, they understand that that’s how the world goes round. If they’re just given the money, then they develop the expectation and that’s what’s always going to happen. The money will just be there if they ask. If you can get them understanding the value of work and the value of money early on, then I think that’s a really good start.

Chores -v- Jobs

Where it gets a little bit more interesting is what you paid them for. I break this down into chores versus jobs. Chores are things that happen on an everyday basis. The trash needs to be taken out, the dishes need to be washed, the laundry needs to be folded. To me, they’re everyday activities that need to happen for the household to function. I personally believe that those sorts of things should be done just as a matter of course. They’re part of a family, they need to contribute as part of their family. They’re doing it for love.

Where they can earn monthly is if you give them different jobs to do, and these are more one-off activities like they might need to clean out the garage or scrub the pool cover or clean the windows or tidy up the attic. Just a specific job that they can get paid for, and you can pay them on an hourly rate. We’ll talk about how much in a minute. So then they understand the ability to earn money according to how much time they spend working on something, or you can just pay them a lump sum. They understand that if I do this particular job, I’m going to get paid X amount of money. This really helps them get into a mindset of they can create value by putting in some effort.

How much to pay children for jobs around the house?

How much should you pay them? Well, it really boils down to how much you can afford and what sort of messages you want to send them about their earning capacity. I think a good starting point is just pay them for their age. We started off when our kids were five, and so we paid them $5. When they were 10, we were paying them $10, and this is a week.

I think it’s really important that if you’re paying your kids for jobs, pay them cash so that it’s tangible. I know we’re hitting headlong into a digital society and possibly they might not be cash around in 50 years’ time but there certainly still is now. If you pay them cash, then it’s tangible. They get to see, if I do the work, this is what I get. With that, they are then able to decide what they’re going to spend the money on.

The Three Jars Idea

I’m a really big fan of the three jars idea. Certainly not my idea. There’s plenty of other people who have this concept or this idea. The three jars are spend, safe, and give.

They can put their money into any one of those, or all three of those jars. I personally think it’s really important that you don’t decide for them which jar they put their money in. They might put it all in spend. That’s fine. That’s their decision they earned the money. However, you teach them that there are consequences of that. If they spend all their money, they don’t have any money saved. If they want something in the future, something that’s going to cost more than what they’ve earned, in that particular week, they’re not going to be able to get it.

You want to teach them about the benefits of giving. It often feels a lot better to give money away to someone else who needs the money more than they do. The love they can feel from doing that and the sense of community and the sense of giving, they’re so powerful, and the feelings, the positive feelings they can get from that can be so much more powerful than spending money on themselves. They need to learn that if they don’t have money saved or put away money to give to other people, they’re going to be missing out on that. You don’t decide for them what they’re going to spend the money on.

However, you do agree who is going to pay for what. If you’re paying them an allowance, you need to decide, are you still going to be buying them ice creams when they go to the movies? Are you still going to be paying for them to go to the movies? Are you going to buy them their clothes or are they going to buy their own clothes? That really comes back to how much you’re paying them obviously, so if you expect them to buy their clothes, then you’re going to have to pay them appropriately.

It’s very important that once you agree who’s going to pay for what, that you then don’t give in when they come to you with their hand out saying, “Dad, can I please have some money?” You go, “No. We pay you money for doing jobs. If you want to earn more money, you need to do some more work.” Then that just cements the concept that if you want money, you have to earn it. I just think that’s really important.

Amy: It’s one of those ideas that’s so simple, and yet, we have to be consistent and purposeful to really make it effective with our kids. One of my children this past year had a regular job and so had regular income, and so I made the transition where for my other kids there’s a set amount of money we’ll spend for buying birthday presents for friends but this year, the child who had that regular source of income coming in began purchasing her own birthday presents for her friends because that was a good simple way to teach her to manage her money.

Although, I will say, my husband, made the mistake one time of offering to pay them per weed. We were going to give this extra job of weeding the natural areas, and he had this great idea. I can’t remember if it was like a nickel or 10 cents a weed, which doesn’t sound too much until you have five very motivated children out pulling weeds. We had to renegotiate that down [chuckles].

Neil: Probably went out and found you had half your garden missing.

What financial topics should teens understand before they leave home?

Amy: Right, exactly. Well, we’ve talked a little bit already about the allowance and teaching our children to manage their money, so we can do that even when they’re younger, and then they get into the teen years. I have teens who I’m just seeing how close it is to the time when they’re going to leave home and hopefully be fully functioning members of society, and they’re going to start getting all those pesky credit card applications in the mail, and we want to set them up for success, so what are the most important financial topics they need to understand before they leave home?

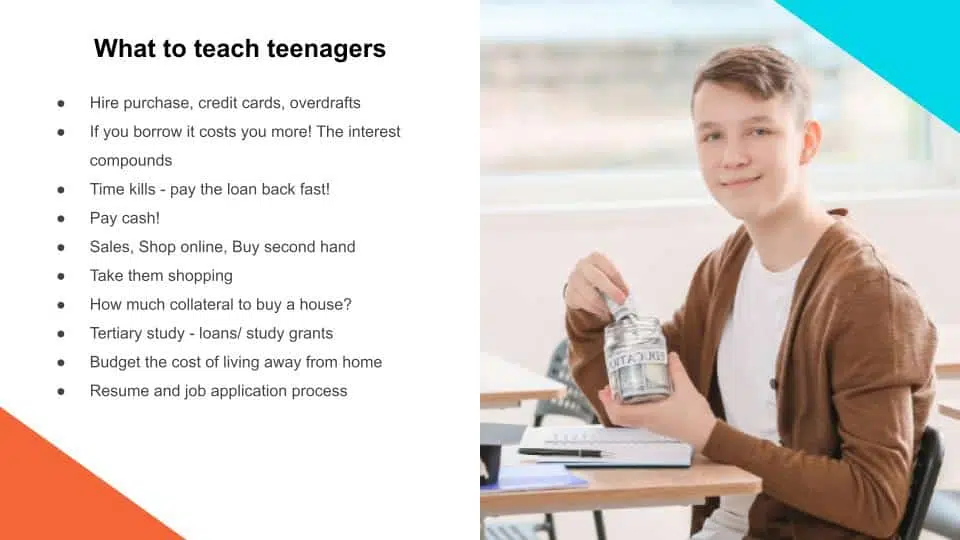

Neil: That’s a really good question, Amy, and that’s one that I’ve had to consider recently with my own kids. They’re all currently or just this year, they’re not living at home, so that was very much on my mind. What sort of things do they need to know right now that they’re starting to go out and live their own lives? As I mentioned earlier on, I think teaching them about debt and the perils of debt is really, really important.

Debt can be good. Debt is fine if you’re borrowing money to acquire something of value, so if you’re purchasing something like a house or some furniture or it’s something that has value, that can be sold if everything turns to custard, that’s fine. You’ve got something tangible for the money. Another form of good debt is if you are investing in your future. What I mean by that is if you’re investing in yourself, are you getting some education that increases your ability to earn more money as time goes on? I consider that good debt.

What bad debt is, is if you borrow money to buy stuff that then disappears. If you borrow money to go do things like go on holidays or buy clothes, which they’re going to get sick of after a while or wear out, if they borrow money to buy presents, that’s bad debt, and so teaching them the difference between good debt and bad debt is a really good start and informing them of the perils of things like after-pay and credit cards and overdrafts because if they borrowed money using these vehicles, it’s going to cost them more in the long run. It’s the purchase price, and then they’ve got to pay the interest, and if they don’t pay the interest off, it compounds, and so it just keeps going up, and that can be a real killer.

The longer it takes them to pay it off, the more interest they’re going to have to pay. So teach them that if they do end up getting some debt, they’ve got to work really hard to pay it back as fast as they can. Tell them what the consequences of not paying it off fast. I’m a great believer of teaching my kids pay cash. My kids don’t have credit cards, so if you can’t afford it, save up for it. I’ve lived on that principle myself all my life. I’ve never bought anything on credit. I do have a credit card, but I pay it off every month, but bigger ticket items like furniture or car or whatever, I’ve always saved up and paid cash.

Then you can teach some things around being smart with their money and how they spend it. Just simple concepts which I imagine they should already have or understand by the time they’re getting ready to leave school, but things like you don’t have to pay full price for something. You can buy it when it’s on sale. If you shop online often, you can get a better deal than if you walk into a store. You can buy things second-hand. A good example, I’m a mountain biker, and I buy a lot of my stuff online, my bikes, my clothes, my shoes. It’s incredible what you can find online, people have bought the wrong size or they don’t like the color or they get injured or whatever, and so they have to sell their gear. You can buy some really good stuff at a fraction of the price than if you’d paid new. A really simple thing that you can do perhaps before they’re teenagers is take them shopping.

Take them grocery shopping with you, and then just think out aloud, “If I buy these beans, it’s going to cost me 50 cents more than these beans. What’s the trade-off? Why is the first can of beans 50 cents more? Am I going to get 50 cents more enjoyment out of the source satisfaction?” Well, maybe, maybe not, but this is a trade-off, that whole cost value exercise but if you’re thinking out loud is you’re making a purchase decision and that helps the child start developing that sort of reasoning and decision making themselves. You have to take a deep breath, especially if you’re taking more than one child. It can get a bit messy if you’re taking a bunch of young kids shopping, but maybe take your partner with you for the support [chuckles].

Another good thing you can teach them is how much collateral they’re going to need to buy a house. I think it’s really important that you talk to kids about the real value of things, say, “In the future, if you want to buy a house, you might have to put $100,000 down as collateral.” They’re going to look at you and go, “That’s just obscene. How on earth am I going to get $100,000?” “Well, you’re going to have to earn it and you’re going to have to set that and save it.” “Okay. Is that even possible?” The answer is, “Yes, of course, it’s possible. You just have to have a plan. Okay, if I earn X amount a week, I’m going to put this amount aside. If I do that for X number of years, I can get to $100,000.” It’s teaching them that big value purchases are possible if they have a plan, and if they have an understanding of the real value of things, that’s going to make the plan a lot more realistic for them. I don’t believe in trying to hide from them the real value of things.

I actually sat down with my son when he left home and we went through a life budget. Saying “Well, if you want to buy a house, this is how much collateral you’re going to need. If you want to have a family, this approximately how much it’s going to cost you per child over a period of time. Per year and then in entirety. If you want to go and travel around Europe for three months backpacking, this is how much it’s going to cost.” These are all back-of-the-envelope calculations. They don’t have to be down to the cent but it just gives them a good sense of “Gee, I shouldn’t be mucking around now with my money. If I want to do these sort of things when I’m a bit older, I’m going to have to knuckle down and earn some money.”

I think that was quite a really helpful listen for him because he was not really in that space. He was just having a good time. Young fellow, first year out of school, first year away from home, having a wonderful time, and not really thinking too much ahead into the future. We sat down and did that exercise with him. He was so grateful for that because he could just see if he carried on what he was doing, he was going to late twenties and he would have nothing to show for then and that was going to take him a lot longer to get to where he wanted to be.

Amy: That is really helpful. I’m glad you were able to have that conversation with him. I think we can probably look back at ourselves being thoughtless or not irresponsible on purpose but just not thinking of those long-term ideas. To be able to sit down and help and mentor our own children in that way is such a powerful gift we can give them.

Neil: It sure is. I’ve got one more thing, Amy. If they’re leaving home, I think it’s really important that they understand how to put a resume together and how the job application process works, how to write a cover letter, because that’s going to– The job they get has a big influence over their earning ability. If they can write a good resume and they can write a good cover letter, they’re much more likely to get a good job that pays well or pays better than a not-so-good job. Just understanding that simple process of a resume and job application can make a big difference too.

Amy: I can see that being something we forget about because we’re just thinking about the cost of things and we forget the other side of the financial equation is upping your income and learning how to do a resume, apply for a job. That kind of thing is going to be a really important tool for them to have as well.

Tips for parents who don’t know how to teach their kids about money

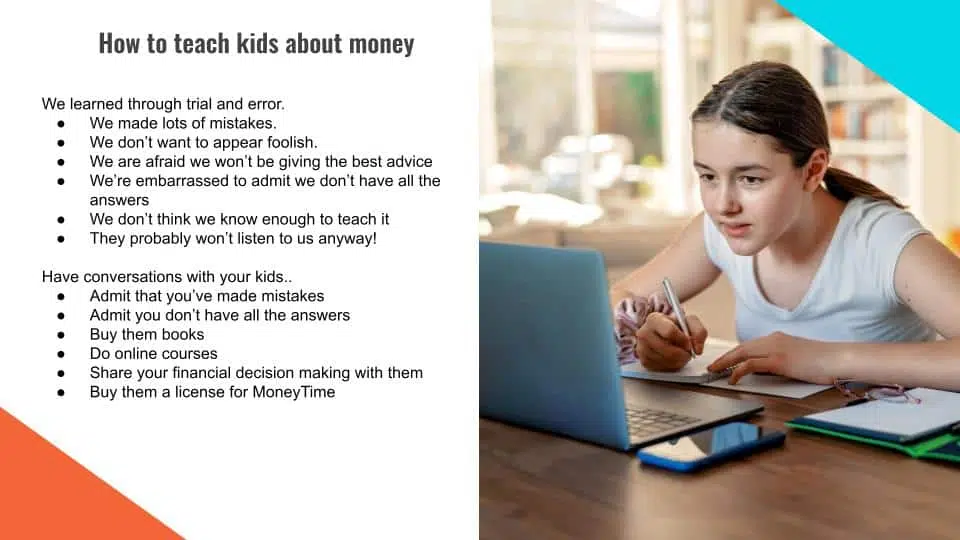

I know that a lot of parents feel really inadequate in this area maybe because they feel like, “Well, I don’t really know what I’m talking about or I’ve made a lot of mistakes or I was never taught.” Maybe for whatever reason, talking about money feels awkward to them. I don’t really feel awkward talking about most things. I love to talk so that hasn’t been an issue. It was my kids and me but I know that can be. I’ve talked to parents for whom that is just really awkward. What are some tips you would give for parents who either feel awkward or inadequate?

Neil: Sure. I’ll just touch on some of the reasons why parents do feel awkward talking about money because this is something that most parents experience and I just want to let them know that it’s quite normal. It’s very prevalent. They’re certainly not alone because most parents had to learn about money through trial and error. We weren’t taught about it when we were kids. We’ve had to learn the hard way. We’ve all made mistakes and we’re afraid to appear foolish in front of our kids when they’re expecting us to have our act together and within a couple of years, we’ll all have enough money to go on SpaceX flights or at least buy the latest pair of Air Jordans.

They’re looking at us thinking, “Why aren’t we doing that? If you’d have had your act together, then we would have been able to do this.” You have to admit, “Well, we made some decisions early on that perhaps weren’t quite so good decisions or we didn’t do things that we could have.” We’re just afraid that we’re going to appear foolish. We’re also afraid that we’re not going to be giving the best advice. We’re not sure that we have all the correct answers. Often we’re embarrassed to admit that we don’t have all the answers. Sometimes we think we don’t know enough to be able to teach it properly. Then to cap it all off, there’s this nagging doubt that they’re going to listen to us anyway. [laughs]

There’s a whole myriad of reasons why parents or many parents find it hard to talk about money to their kids. Just want to say, don’t worry about that. You’re absolutely not alone. It’s quite normal. In actual fact, it’s not that hard. Here are some conversations or things that you can have or do to teach your kids about money. Just simply have conversations with them about money. Admit that you’ve made mistakes. Talk about some of your mistakes. Why have them go through the same experience to learn the same lesson? Why not share with them your mistakes?

We’ve had full ownership of our house for, gee, 15 years, but we’ve never done anything with the equity in the house. We could have gone off and borrowed money and bought another house but we didn’t. If we’d done that 15 years ago, we could have had three houses by that, three investment properties, but I didn’t do that. I didn’t know how to do that. I didn’t think I could. I just thought that was something that other people did. That was a mistake that I’ve made. I’ve had to admit to my kids that I don’t have all the answers.

I have learned an awful lot through the process of creating MoneyTime. I’ve learned a lot about money management and personal finance stuff that I didn’t know before, but I have to admit to my kids, “Before I did MoneyTime, I didn’t know much more than they do.” The first thing I think you can do is just, just make it fun. Games like Monopoly or Risk. It’s very non-threatening. It’s just a fun game that you can start introducing them to principles like mortgages and debt and property and getting money.

You can buy them books like Robert Kiyosaki’s Rich Kid, Smart Kid. That’s a great start. It was just a really good, simple, easy to read book. Over here in New Zealand and Australia, there’s the Barefoot Investor. There’s a book called The Barefoot Investor for Families which I think is excellent. It’s written by Scott Pape. He’s an Aussie with a great sense of humor, really down-to-earth advice. It’s a fun read. I read it cover to cover in a day. It’s an easy read but just really good practical advice on how kids can manage their money.

You can encourage them to do online courses. You can do online courses yourself. There’s all sorts of courses you can find on the internet these days if you just search financial literacy or teach or learn financial literacy. There’s an abundance of courses and podcasts you can access. I think from a day-to-day or practical perspective, share your financial decision-making with them. If it’s the end of the month and it’s time to pay the bills, you get them to sit down with you and go through the process with them and say, “Look, this is how much our utilities are. This is how much it is for the gas. This is how much it is for the power. This isn’t how much it is for our property tax.”

They go, “Oh gee. We don’t really. We pay for that? What does that money go for? What is property tax? Why do we pay that? What does the council or the government do with that money?” It’s just simple day-to-day financial decisions. If you include them in on those, then it becomes part of normal. It’s not a scary concept, it’s actually this is just how life works.

Then finally, and possibly the easiest thing you could do is buy them a license for MoneyTime. [chuckles]

What makes MoneyTime unique?

Amy: Yes. [chuckles] Well, tell us a little bit about MoneyTime. We’ve heard about why you created it, but how is it set up, and what makes MoneyTime unique?

Neil: Sure, thank you. I’ve spent the last four years of my life developing and writing and promoting this program. It’s an online program, it’s web-based. It’s 100%, self-directed, which means that the child can go through the whole program, without any assistance from a parent.

It’s specifically designed for 10 to 14-year-olds, I mentioned earlier, this is the time that we think it’s most important to build good habits and ideas around money. That’s the age group that we’ve targeted. It’s very age-appropriate. All the examples in the program are specifically targeted at 10 to 14-year-olds. The situations that a 10 to 14-year-old can relate to.

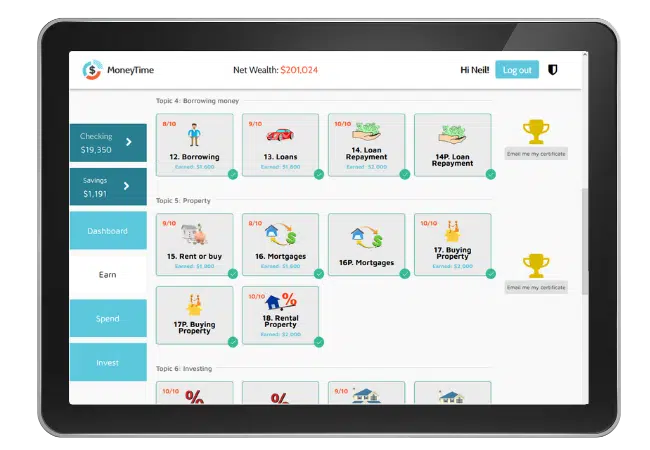

Because it’s all self-taught, it doesn’t require the parent to have all the answers. A parent can be involved as much as they like, we have some module guides that we provide with the program that the parent and the child can work through, together with, if you want, you can be involved in the process as much as you want to be. If you don’t want to be, and you’re not sure what you should be telling them, just let the program do it for you. It’s very comprehensive. It starts off from how you earn money, you can put into a bank and earn interest.

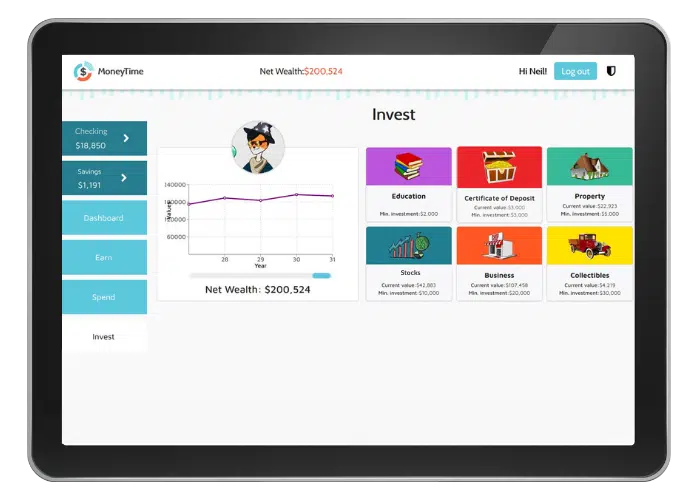

Once you’re earning money, you should be thinking about doing a budget so that if you spend less than what you earn, in a week, you have money aside that you can save. Then we talk about how to make good purchase decisions, talk about different ways of banking, and paying for things. We then get into what they can do with the money once they have saved it and that gets into we talk about buying property, the process for buying property, what it’s going to cost them. We talk about collateral, and sorry, down payments, and we talk about interest and paying off mortgages.

Then we go into investing, it’s another thing they can do with their money to grow their money. They can put it into CDs, or they can invest it in stocks, or they can invest it in a business. We talk about the different rates of return for each of those investments and the risk involved with those. It sounds like it might be perhaps over the head of, say, a 10-year-old, but what I’ve done is sat down and assume that they have zero knowledge to start with. I have explained it in really simple terms, what these things are and what it means. It’s amazing how much the kids absorb this information and they are able to understand it.

We do regular testing throughout the program and on average, students gain a 43% increase in knowledge across the whole program. We know that we’ve nailed it in terms of age-appropriateness, and putting things in a way that the kids can understand.

Two of the key principles or ideas that we promote within the program, that having money is a good thing. A lot of people or some people have issues around wealth and for some it has negative connotations of having too much money or having lots of money. Well, we don’t agree with that.

We think that having money is a good thing because it gives you choices. Choices to do things for yourself, for your family, for your community, and for your church. If you have money, then you have options. You have opportunities to do good things with it.

Secondly, we teach them the basic principle that you budget to save and then you save to invest. That’s the approach that everybody should be taking with their money if they want to improve their net wealth. In the program, we show them how they do that, how they can do that. It’s really simple. It’s also a lot of fun because we’ve gamified it, it’s not just a bunch of lessons. We’ve gamified it. They have an avatar, they can go shopping for their avatar in different shops.

The shops unlock as they go up through the different levels of the program, they can donate money to charity, and they can win generosity medals for doing that. They can transfer their money into a savings account earn an interest, or they can invest it. There’s half a dozen investments that unlock as they go up through the program, they can invest in their education, and get a better paying job. They can invest in CDs, stocks, property, and collectibles, these are things like antiques. We just threw that in for a bit of fun.

What we are giving them is an opportunity to make financial decisions, and see what the consequences of those decisions are in a fun way.

At the end of the lesson, they’ve made some money from doing the quiz, they then get to decide what they’re going to do with the money, are they going to spend it? Are they going to save it? Are they going to invest it? Are they going to give some money away? These are the decisions they’re going to be having to make as an adult or as soon as they have any real meaningful money of their own. These are the decisions that they’re going to have to be making.

We’re giving them this opportunity to make the decisions now, within a game in a safe environment where there’s no penalty for failure, other than their sibling looking over their shoulder and going, “Oh, you Wally, what did you put your money in that for?” “I put my money in this and look at my net wealth now.”

That’s the key approach that we’ve taken is, by gamification, we’re giving them some experiential learning. The kids love it. Like you mentioned, right at the beginning, the program is being done by 35,000 kids now. We have really great feedback from parents and from teachers and schools. They love using the program because it is self-taught, that takes the pressure off them. We’re just absolutely delighted with how it’s going and the results it’s getting.

Amy: Well, I think that MoneyTime would definitely be such a great part of a homeschool family’s weekly schedule. I got a chance to look at it and do some of the first lessons looking over my 10-year-old daughter’s shoulders.

One of the things I really loved about it was that it started so simply so that even when she took that there was like a pre-test to see what you knew already and what you didn’t know. Seeing things like, “oh, I guess I thought you knew that. I guess you didn’t.”

From the very beginning it’s easing you in, but then the later lessons are talking about important things. It doesn’t just stay at a low child level. I felt like it was going give some real depth to the lessons.

Then I also really appreciated that perspective on money as being something that gives you choices. It gives you freedom, it’s not just about like accumulation so you can go buy stuff, or it’s really about that freedom that it gives you to choose things about your time, to choose the way you spend, and give and save and all those things. I think that’s a really, just a good foundational perspective to have. I don’t know, I think parents might find themselves learning a lot too, as they watch their kids.

Neil: [chuckles] Well, I’m sure they do. In fact, a lot of parents have said to me, “Gee, can I do it?” [chuckles]

Amy: Sure. [chuckles]

Neil: Of course I can.

Amy: That’s great.

Neil: It’s interesting that the thing about starting right at the very beginning, assuming that the kids don’t know anything, when I first wrote the first three modules, I tested them out on on some kids at a school. I was really surprised at how little they knew. I assumed that they’d know the difference between a checking account and a savings account. I assumed that they’d know what interest was. No, they don’t. They didn’t. These were 10-year-olds, they didn’t know. I thought, Oh, I’d spent three months writing these three lessons because I was figuring out how to structure at all, I had to go back and rewrite them. [chuckles]

Amy: Wow.

Neil: That paid dividends because I could see them from my testing from then on I sat with– I did 121 one on one sessions with kids in the school, half an hour each going through the program, seeing what they enjoyed, seeing what they understood, watching their body language, did they get onto a screen and start scratching their head, or did they smile or did they laugh? Did they know immediately what to do next? I got a really good appreciation of how well the kids were understanding and enjoying the program. That’s borne fruit because we get such great feedback from the kids. They love doing it. It’s fun.

I get a lot of teachers from schools saying MoneyTime is their favorite thing that they do in the week. She says, “I have to swap them away. No, we’re not doing MoneyTime right now. We’ve got something else to do, but you can do it later on,” which is just such a good feeling for me having invested so much of my own time into putting it together, to know that it’s having that sort of impact on kids. It’s very heartwarming.

Amy: Screen time, but the parents don’t have to feel guilty about it because it’s actually an investment in their children’s future. If anyone is listening, within the first couple of months of this podcast episode publishing, I did want to let you know that MoneyTime is running a 25% off discount on their annual membership through the end of October. I will have the link so that you can access that in the show notes. Be sure to check that out.

Neil, this has been such a delightful conversation. Thank you for taking the time to chat with us. Here at the end, I’m going to ask you the question I’ve been asking all of my guests this season, and that is just, what are you personally reading lately?

What is Neil reading lately?

Neil: Well, Amy, I’m reading a book called The Dice Man by Luke Rhinehart. It’s a book about an American psychiatrist who’s in his 40s, and he’s bored with life, and he decides to spice it up by throwing a dice every time he has to make a decision. That leads to some really interesting consequences because he doesn’t hold back on the things that he’s going to decide about. It’s like he’s spiraling down into madness with this, but he also seems very lucid at the same time with this rationalizing. It’s in first-person. You follow him on this journey. Is he quietly going insane or is that just a very rational experiment that he is taking to the extreme? It’s a fascinating book. It’s extraordinarily well-written.

Amy: It sounds like it would make you ask a lot of deep questions and twist your mind up a little.

Neil: It really does. It has you starting to wonder about some of the conventions that we live with, and the norms, and the expectations that society puts on us. If you shared all of those, how would your life be? It does ask some quite probing questions, or you find yourself asking yourself some pretty probing questions. What would I do? Would I be prepared to do that? The answer is, no, in most cases.

Amy: Yes, seriously, I was going to say. [laughs] I don’t know. I’d have to be in a real healthy mental state to read a book like that. Neil, thank you so much. Those who are listening or watching, be sure to check out the show notes where I will have links to the things that Neil and I have chatted about. You can find all of the links as well as the slides that Neil prepared over in the show notes as well at www.humilityanddoxology.com. Thanks, Neil. Have a wonderful rest of your day.

Neil: Thank you, Amy. It’s been a pleasure.

Find MoneyTime Online

- Facebook – @moneytimekids

- Instagram – @moneytimekids

- Twitter – @MoneyTi16929931

- YouTube

- Pinterest – @moneytimekids

You may also enjoy these Homeschool Conversations:

Check out all the other interviews in my Homeschool Conversations series!